Compiled by Walter Sorochan

Posted April 15, 2017; updated November 14, 2021.

In the good old days and even today, churches, communities and towns kept local records of everything of importance: the buying and selling of goods; births, marriages, and deaths; loans; election results; bank records, real estate transactions, property deeds, legal rulings; and anything else of note. Keeping such records took weeks, months and even often years to transact and record and these were usually expensive. Records had to be moved from place to place and involved many middle-men in the process, adding to the expense. Records were centralized, like being kept at a bank or real estate office, and usually of public record, with no privacy.

All this old time recording is about to change with an internet system called blockchain. This radical new record-keeping and money system is going to change how we buy groceries, pay our bills, and conduct business. It could even completely eliminate paper money.

A revolution in the making

To understand the revolution about to take place in money, finance, information and business transactions on the internet, you need to understand blockchain and bitcoin.

|

Blockchain offers a way for people who do not know or trust each other a way to create a record of who owns what that will force the agreement of everyone concerned. It is a way of making and preserving truths. A blockchain, as the name suggests, is nothing more than an ever-lengthening chain of blocks of data. Each block contains a compact record of things that have happened. How it does this is interesting and complicated. The important point is that if something is recorded in a blockchain, it’s deemed by users to be true with a capital T. |

We start with bitcoin.

This

revolution started with a new fringe economy on the Internet: an

alternative currency called Bitcoin. Bitcoin is a system designed to

create a truly free, open, fair, equal, decentralized & borderless

network to facilitate trade between only two parties that matter in a

transaction. A transaction system without buildings, owners or

employees, in which everyone can open an account, that does not require

identification and is completely free. This is a system without any

arbitrary borders, fees, restrictions & regulations.

This

revolution started with a new fringe economy on the Internet: an

alternative currency called Bitcoin. Bitcoin is a system designed to

create a truly free, open, fair, equal, decentralized & borderless

network to facilitate trade between only two parties that matter in a

transaction. A transaction system without buildings, owners or

employees, in which everyone can open an account, that does not require

identification and is completely free. This is a system without any

arbitrary borders, fees, restrictions & regulations.

Like paper money and gold before it, bitcoin is a currency that allows parties to exchange value. Unlike it predecessors, bitcoin is digital and decentralized. For the first time in history, people can exchange value without others [intermediaries] which translates to greater control of funds and lower fees. Bitcoin makes banking outdated and unnecessary.

But

there could be a problem with just using bitcoin. With Bitcoin, there

may be a risk that the holder could just send copies of the same bitcoin

token in different transactions, leading to “Double-Spending”. This is

where blockchain comes in to stop the possibility of double-spending.

But

there could be a problem with just using bitcoin. With Bitcoin, there

may be a risk that the holder could just send copies of the same bitcoin

token in different transactions, leading to “Double-Spending”. This is

where blockchain comes in to stop the possibility of double-spending.

Blockchain technology helps counter issues like double spending. The simplest way to think of blockchain is as a large distributed ledger [ accounting chart on left] of sorts that stores records of transactions. This “ledger” is replicated hundreds of times throughout the public network so it is available to everyone. Every time a transaction occurs, it is updated in ALL of these replicated ledgers, so everyone can see it.

.

The illustration above summarizes blockchain. Every time a new transaction is initiated, a block is created with the transaction's details and broadcast to all the nodes. Every block carries a timestamp, and a reference to the previous block in the chain, to help establish a sequence of events. Once the authenticity of the transaction is established, that block is linked to the previous block, which is linked to the previous block, creating a chain called blockchain. This chain of blocks is replicated across the entire network, and all cryptographically [scrambled computer code] secured.

The blockchain is a giant ledger [record keeper] that keeps track of who owns how much bitcoin. The coins themselves are not physical objects, nor even digital files, but entries in the blockchain ledger: owning bitcoin is merely having a claim on a piece of information sitting on the blockchain.

Units of currency are transferred from one party to another as part of a new “block” of transactions added to the existing chain—hence the name. New blocks are tacked on to the blockchain every ten minutes or so, extending it by a few hundred lines.

The same could be said of how a bank keeps track of how much money is kept in each of its accounts. But there the similarities end. Unlike a bank’s ledger, which is centralized and private, the blockchain is public and distributed widely. Anyone can download a copy of it. Identities are protected by clever cryptography [scrambled computer code]; beyond that the system is entirely transparent.

A blockchain facilitates secure online [internet] transactions. This blockchain-based exchange of value can be completed more quickly, more safely and more cheaply than with traditional systems. A blockchain transaction, such as buying a house or other real estate transaction, can be completed in four hours or less time; compared to today's house buying time of a month or longer.

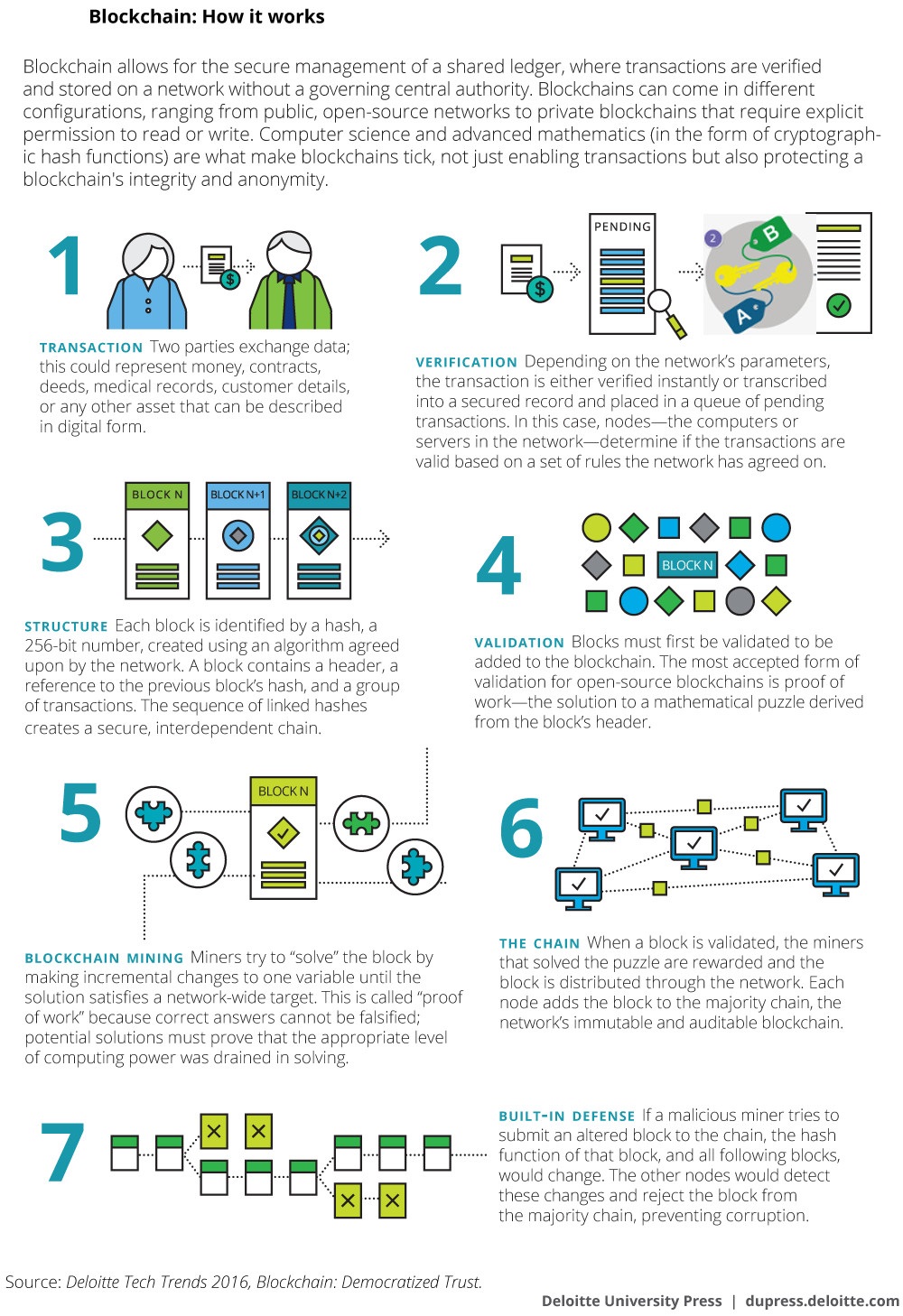

The data records, which can be a Bitcoin transaction or a smart contract or anything else for that matter, are combined in so-called blocks. In order to add these blocks to the distributed ledger, the data needs to be validated by 51% of all the computers within the network that have access to the Blockchain.

The validation is done via cryptography, which means that a mathematical equation [scrambled computer code] has to be solved. Solving the mathematical equation is difficult and requires a lot of computing power. However, once it is solved it is immediately clear that the answer is correct. This can be compared to a crossword puzzle, which can be very difficult to solve, but once completed you immediately know that it is done correctly.

Once the validation is done, the Block will receive a timestamp and a so-called hash [The block hash [e.g. #] identifies a block uniquely and unambiguously]. This hash is then used to create the next block in the chain. It is nearly impossible to change data that has been recorded on the Blockchain.

Advantage of Blockchain: A blockchain facilitates secure online transactions. It is able to keep electric power distribution, water treatment, self-driving transportation, and much more from ballooning beyond all practical limits as cities continue to grow. With a robust public blockchain in place, cities could provide payment options for every business — why use your old plastic card, losing a fraction of the payment to an intermediary middle-man like a bank or credit card company and driving up the price, when you can transfer money quickly and securely, directly to the person you own money to or to a business owner?

Companies could make online payments more secure and inexpensive. Blockchain can be used safely between countries and institutions to transact business quickly, safely and for less cost. Current day scams using internet credit card would be eliminated!

Individuals might use blockchain technology to take control [privacy] of their own medical records in a secure “distributed medical records system”.

People would be able to transfer money without a bank or write enforceable contracts without a lawyer or notary. Fewer bankers and lawyers!

There is gossip about cash dollar money being replaced by a new form of credit card. It could very well happen that you go grocery shopping and pay without cash or credit card. Will it be blockchain?

A blockchain database consists of two kinds of records: transactions and blocks. Blocks hold batches of valid information that are hashed [#] and encoded into a Merkle tree [ merkle tree root, a data structure used to efficiently summarize all the transactions in the block. ]. Each block includes the hash of the prior block in the blockchain, linking the two. The linked blocks form a chain. This iterative [repeating] process confirms the integrity of the previous block, all the way back to the original genesis block.

Be prepared to have your bank checkbook and credit cards replaced by blockchain.

Is blockchain a dream? As of September 17, 2015, the following banks [below] are planning to develop and implement Blockchain-like Technology:- JP Morgan

- Commonwealth Bank of Australia

- BBVA

- Barclays

- Goldman Sachs

- UBS

- Royal Bank of Scotland

- Credit Suisse

- State Street

The first cross-border transaction between banks using multiple blockchain applications has taken place, Commonwealth Bank of Australia and Wells Fargo & Co said on October 24, 2016, resulting in a shipment of cotton to China from the United States. Kaye: Bank uses blockchain

References:

Coy Peter and Olga Kharif, "This Is Your Company on Blockchain," Bloomberg Business Week, August 25, 2016. Article by Coy: Bloomberg blockchain is no longer active.

Crosby Michael et la., "Blockchain technology," Sutardja Center, UC, Berkley Engineering, October 16, 2015. Crosby: Blockchain tech 2015

IBM, "Making blockchain real for business," January 16, . IBH: Blockchain business

International Banking, "The next big thing," The Economist, May 9, 2015. International banking: Blockchain 2015

Kaye Byron, "Major banks mark first-ever international trade using blockchain tech," Reuters COMMODITIES, October 24, 2016. Kaye: Bank uses blockchain 2016

Rijmenam Mark van, "What is blockchain and why is it so important?" Datafloq, Rijmenam: what is blockchain