By Timothy Rand

Money can be anything that is widely accepted as “payment” for products and

services.

Excessive and unsound lending in the United States Banking

industry in the last few decades might result in a complete

financial system reset.

So let us explore the nature of money itself.

In all modern monetary systems, money is supported by debt, or more precisely, the collateral backing that debt. Whenever a saver deposits his hard-earned dollars in a bank, the bank turns around and lends these same dollars out. The saver's deposits are only as valuable as the collateral behind these bank loans.

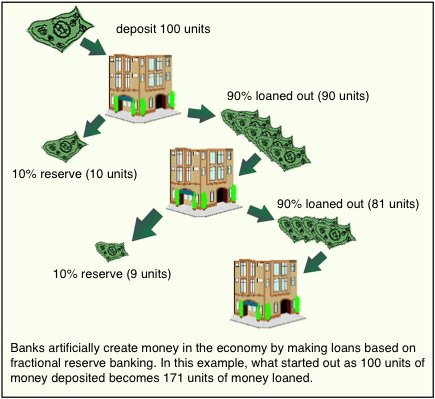

Perhaps one of the greatest economic innovations in history has been the development of a fractional-reserve banking system. Before the invention of banks, money usually took the form of unique physical assets: gold, silver, grain, shells, or anything rare, long-lasting, valuable, and hard to counterfeit. The one commodity that has stood the test of time is gold, so Rand uses that as his base case of "hard money". One of the problems with the "gold as money" system is one of liquidity. There is a massive amount of wealth and wealth-generating potential in the world --- such as real estate, land, labor, inventions, trade, etc., - but only a limited amount of gold. Before the days of banks, to convert any of these things to spendable cash, you would have to locate and convince someone with surplus gold to lend some of it to you, or else bide your time until you had earned enough gold to consume or invest on a significant scale. Economic progress in such a system is slow, as the liquidity required to make long-term investments is confined to the very few who possess excess gold reserves.

On the other hand, fractional-reserve banks greatly expand the money supply by creating a brand new type of money: the bank note. Banks accept deposits (originally gold), and then take these funds and lend them out as bank notes [Federal Reserve Notes in our current system]. The banks only keep a fraction of their total deposits as a reserve against future withdrawal. The saver in this system may actually believe his deposit is liquid and readily available, when in fact it has been loaned out by the bank and is not - in aggregate - readily retrievable. This liquidity mismatch is both a great engine for economic growth and the potential fly in the ointment of the entire enterprise. Banks expand the money supply by literally creating and redefining money: rare physical gold is supplanted by collateralized banknotes as the new "legal tender for all debts, public and private."

The great power of banks is the expansion and democratization of money. Many forms of wealth and wealth-generating enterprise - not just gold - can be converted to spendable cash by borrowing from a bank. Furthermore these borrowed funds are treated as newly created money that adds to the overall money supply. For example, a home equity loan can be obtained to convert a homeowner's existing home into spendable cash, a mortgage can be obtained to convert a worker's future income stream into the spendable money needed to buy a brand new home, a small business loan can be obtained by an entrepreneur to start a new enterprise. In each of these cases, the overall money supply is increased as the borrower spends the proceeds from his loan, and the ultimate recipient deposits these same bank notes as newly found money into his bank.

With the rise of fractional-reserve banks comes the phenomenon of "debt-financed expansion." Through bank-enabled financing, entrepreneurs are able to borrow against collateral and/or future income to buy houses, expand businesses, and start new ventures. As the money supply grows, there is more than enough liquidity available to pay off debt service, hire new workers, and garner profits. It is a virtuous cycle that ignites the "animal spirits" and drives economic growth.

One of the problems with fractional-reserve banking, however, is that once the overall debt level reaches a saturation point, the liquidity mismatch at the heart of the enterprise rears its ugly head, causing instability and a potential reset. When the debt levels reach a critical and unsustainable level, newly issued loans can no longer be supported and the money creation phase of the expansion grinds to a halt. Suddenly depositors need to withdraw money en masse to pay off their accumulated debt service. Since the liquid money is not even available to the bank (since it has been converted almost entirely to long-term mortgage loans), panic sets in and a bank run can happen.

One of the open questions as we progress through our current financial crisis is whether our debt-based monetary system has reached (or over-reached) its carrying capacity for debt. A second question is whether our financial system is even salvageable in its present form if indeed it has reached its limit.

The above mumbo-jumbo about money adds to the confusion about money. This author has tried to unravel the hidden mysterious source of money in the article "Currency Market, The Money Cartel & World Economy" Sorochan: 2019

The chain of command of money: The money cartel controls the Bank for International Settlements [BIS], the International Monetary Fund [IMF] and the World Bank; all private entities that are not free markets. These are monopoly entities [no competition] that are under the control of the international cartel, that facilitate the movement of money and that lend money to central banks of national governments and private enterprises. The only thing that the government controls is how many dollar bills it will print. The more money the government prints the deeper the government goes into debt!

Gold dust blinds the dollar: All the above information about the nature of money is nice to know but let's look at the reality of money and the economic system today, in 2019. The government borrows paper money notes from a private entity, International Monitary Fund [IMF] and disperses the money to the government Federal Reserve Bank, as a promisory note to be repaid with interest. This allows the government to print promisory paper notes as dollars in the demominations of $1, $5, $10, $50 and $100 bills. These government dollar bills have no collateral to back them up. As long as the government keeps printing these dollar bills out of air, this allows the government to spend and spend money that becomes a debt to the IMF. These are added as debt to the country.

But before 1972, the government used gold as a collateral to back up the paper dollar bills. President Nixon removed gold as required collateral but kept gold tied to the dollar. If the dollar value of gold rose, the dollar bills were devaluated and visa versa, when the gold dropped in value, the dollar value went up. That is what has been happening for the last 20 years. It seems that someone may be manipulating the entire US monitary system; trying to keep the economy from crashing!

Should the US and world economy go into a recession, there is talk of bringing gold as a standard of exchange back and allowing it to float in the free market world. Gold would replace paper money as a media of exchange. The rational for such thinking is that the value of gold always retains its luster and value, not like wheat, corn, cars or lumber that can rot over time and become dust. Gold stays as gold, regardless of how you divide it. Silver also has similar long-term value. But other metals like iron ore can rust over time. Money may even become a bartering system, like getting paid for work done in exchange for eggs and food of equal value. Today's money is a debt system, it depreciates very qyuckly and it is unstable as a media of exchange. You can easily check this out for yourself by comparing the value of a US dollar in 1900, what it will buy then, and compare it to 2019 today. It would be nice to buy an icecream cone for 5 cents instead of 5 dollars.

So .... the dollar money may be replaced by gold as currency money. Yes, speculation but a real possibility.

References:

Kaluza Lukas, "Essays on monetary theory and policy: on the nature of money (9)," New Economic Perspectives, December 29, 2013. Kaluza: Thew nature of money 2013

Rand Timothy D., "The Nature of Money," January 23, 2010. Article by Rand: nature of money is no longer active.

Wray L. Randall, "MMP #52 Conclusion: The nature of money," New Economic Perspectives, January 23, 2010. Article by Wray: nature of money is no longer active.