|

Simplified by Walter Sorochan, Emeritus Professor: San Diego State University Posted 2008; updated November 2021. Speculative gambling on the stock market started big time in the late 1980’s with Enron. Enron, the defunct energy corporation in Houston, Texas., evolved its own form of an unregulated banking and loan system. Enron borrowed the idea of a new instrument from JPMorgan Chase Bank in the early 1980s; that exchanged or swapped paper debt for collateral. The new instrument was called the Credit Default Swap [ CDS ] and was used as an insurance to secure paper notes or loans and also generate income for Enron.

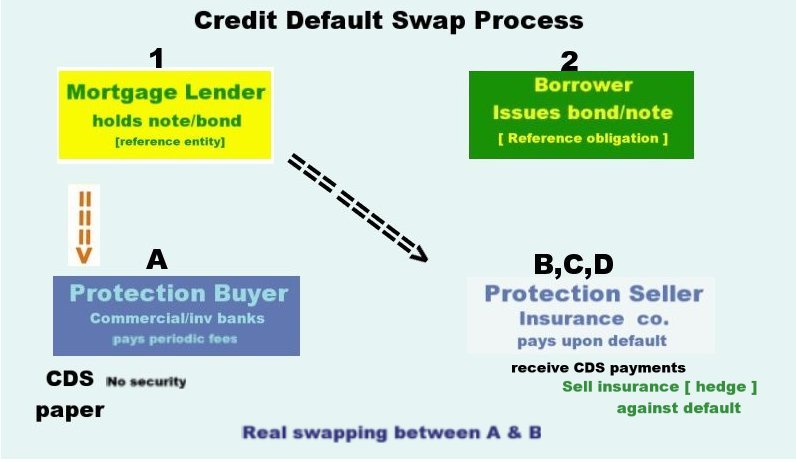

Enron envisioned the primary benefit of the credit default swap as a new source of risk distribution. But the real motivation for Enron [ and banks ] to use CDS was to create unsecured money. Enron sold paper notes or derivatives to its own 3000 subsidiaries as a way of generating small amounts of cash with each transaction. This pyramid scheme worked as long as new investors were continually sucked in at the bottom to support the investors at the top. Enron ran into trouble when a speculator of “ a note “ made a call [ requested payment ] on the original paper note. Enron did not have enough cash on hand to pay for the entire note and had to declare bankruptcy. Enron evolved an unregulated, secretive and confusing Punzi scam for making money. Using the above information about Enron as a starting point, we provide more information about what Credit Default Swap is and how it works. Instead of holding the collateral home as security until the owner paid the loan off, the new instrument for the loan allowed banks to sell or “ swap ‘ their collateral [ e.g. a borrower’s home ] to another company in exchange for paper equity. The new instrument was called the Credit Default Swap [ CDS ] and it was used by big loan and commercial banks as a way of insuring loans. The CDS became an insurance policy against a failing loan. Since, 2000, Banks dangled CDS, like a carrot to catch a rabbit, to attract buyers when they had a hard time raising cash. Big banks used CDS as a way to raise cash and thereby have more cash to loan out. What is a Credit Default Swap or CDS? [ 30 ] CDS is a contract by the protection buyer, usually a big commercial or investment bank [ buyerA in illustration below ] for a CDS note or bond from a lender # 1. The Protection Buyer uses the Credit Default Swap as an insurance or hedge against possible default by the #1 Mortgage Lender that created the CDS. A CDS is not cash, it becomes a paper of debt contract. [6. Shedlock, Mish ]

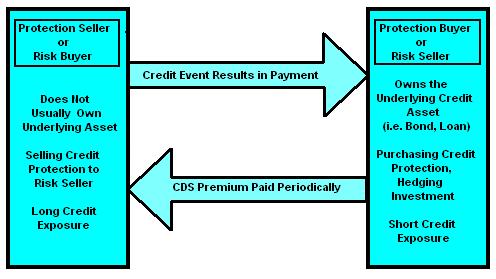

This contract is initially sold to a Protection Seller [ B in the illustration above ] in exchange for an insurance policy. Protection Seller B can sell this paper note to another Seller C, who in turn, can sell the paper to D and so on ] The current speculation in oil and other commodities in the stock market has speculators betting or hedging on the pricing or future availability of the commodities, thereby driving the price of the commodities up while at the same time getting rich. How does this contract work? Lets look at how CDS protects the Protection Buyer bank [ A in above illustration ] issuing the contract. The bank creates a contract to buy insurance against it defaulting on borrowed money. An insurance company [ B, C, D, etc. ] or Protection Seller agrees to buy the bank contract on the assumption that it can make money by selling it to another party for a profit. Such purchase becomes a source of income to the bank. In return for the insurance coverage, the bank pays a “ premium “ amount, usually 10 % of the CDS value.[ 36. Pearlstein: good explaination of CDS ] The real swapping of CDS paper note takes place between Protection Seller and Protection Buyer, as illustrated in the diagram below and above.

The buyer of the insurance makes periodic payments to the Protection seller [ a bank ] and in return obtains the right to sell a bond issued by the reference entity for its face value if a credit event [ like a default ] occurs. By issuing CDS as a contract and allowing the buyer to take the risk of the CDS, the bank usually has more cash on hand to make more loans. This scheme works as long as the originator of the CDS does not have a major run on this debt and the bank can keep getting more persons to take out a loan and pay premiums. How worthy is the CDS contract? Things got totally insane when the credit markets allowed interest on bonds to be paid not with cash but with issuance of still more paper debt. Debt was paid back with more debt with discounts at each transaction! Thus, the real liquidity value of a big bank selling a CDS and using it as accounting for cash becomes questionable and suspect. A CDS is not cash, it is a paper of debt contract. [6. Shedlock, Mish ] The original CDS is usually discounted from 3 to 10 or more percent. As the CDS note is bought by transformers [ second buyer, this buyer to a third and so on ] down the line, there is usually a discount in the value of the CDS note. The value of each transactional sale may be discounted or increased in value, without previous holder’s knowledge. Since the value of a CDS is not standardized, there are usually differences in the real value of a CDS contract from buyer to buyer. You can estimate just how risky a bank is by the amount of interest it pays its customers. The higher the interest rate, the riskier the bank. For example, Kaupthing, the major bank in Iceland, was paying about 11 percent return on deposits when it had a CDS value of 833 basis points or bp on March 17, 2008. After Bear Stearns Bank collapsed, the CDS rating for Kaupthing bank on April 01, 2008, rose sharply to 1000 bp for one-year contracts, with the interest climbing to 15%. The interpretation of the interest rate rising to 15 % is that the bank needs more cash in order to attract investors. This high interest rate also indicates that insurers of bank debt consider this bank to be a very high failure risk. Bank Risk: A good example to illustrate bank risk is to examine the American bank, Washington Mutual [ WM]. On March 3, 2008, this bank had a credit default swap spread from 468 basis points to 550 basis points. This new increase would have cost Washington Mutual $550,000 per year for five years to insure $10 million in debt. But from a customer point of view, Washington Mutual, during this time period, would pay almost double the interest paid by more solvent banks. A customer would be attracted to open an account at WM not realizing that the higher interest rate meant a higher banking risk. Mid-March contracts on Seattle-based Washington Mutual increased to a near-record 644 basis points, according to CMA Datavision. [ no link ] With the infusion of new cash in early April, 2008, the five-year debt insurance costs on Washington Mutual fell to about 302.5 basis points, or $302,500 a year to protect $10 million of debt, according to data from Markit Intraday. [ 14. no link ] [ The interest rate % paid its customers for depositing at WM dropped substantially at this time. ] Power of CDS over Stock market: Credit Default Swap and its derivatives are unregulated. The unregulated market in credit default swaps has twice the face value of the US stock market. It is bigger than the USA NYSE and behaves like a wild west shootout! Consequently, it should not be a surprise to hear rumors that the bailout was necessary to save wall street from a stock market crash bigger than that of 1928. [17. Brock ] Conclusion: A huge pyramid of debt was made possible by thirty years of relentless deregulation of financial markets. A new system of “ swap “ banking and loaning was evolved that helped banks and loan institutions make money. It spreads the risk of failure to other parties. The entire monitory system allows all parties to be able to gamble on the loans created. It is most unfortunate that in the lust for money and power, the bankers and their governments have lost their old fashioned values of right and moral good. We appear to be evolving from free wheeling capitalism to regulated socialism in the banking system. Greed for money and power does not regulate itself! The trouble with credit-default swaps is that these are thinly traded, have huge counter party risk, are unregulated, difficult to analyze, have shoddy book-keeping [as off-balance-sheet operations ] and are difficult to monitor. Contracts can be traded or swapped from speculator to speculator without anyone overseeing the trades to ensure the buyer has the resources to cover the losses if the paper note defaults. The instruments can be bought and sold from both ends — the insured and the insurer. The system uses debt as ‘ hollow ’ credit that has no security backing it up. Banks sell their debt and use it as credit to get money so they can become more solvent. Schwartz [ 20. no link] has argued that CDS is not insurance. This raises the validity of using insurance to indemnify CDS. To the extent that CDS is being sold as “insurance,” they are looking more like insurance fraud; and that fact has particularly hit home with the ratings downgrades of the “monoline” insurers and the recent collapse of Bear Stearns, a leading Wall Street investment brokerage. The monolines are so-called because they are allowed to insure only one industry, the bond industry. [ 35. Brown ] The International Monetary Fund said in March, 2000, that banks were in the worst financial crisis since the Great Depression. [ 21. Pittman ] The tragedy of Enron is that governments and banking institutions did absolutely nothing to stop the tragedy from reoccurring. The Enron tragedy resurfaced again in 2008. [ 30. Enron tragedy ]

The big banking firms of United States had forced the world banking institutions to play their swap game. It is a travesty that the global swap banking game has endangered the security of countries and their monetary institutions by participating in questionable banking schemes like swap derivatives. The demise of Enron and Bear Stearns will continue to swallow not only banks, but countries globally, simply because CDS is a bad Punzi gambling scheme for making money! The unregulated swaps game is now endangering the world food and oil supplies by allowing swaps to impact commodities [ grains, rice and other foods ]. Wall street speculation has driven the price of crude oil to $ 138 a barrel on June 6, 2008, and raised the price of gasoline to over $ 4.oo a gallon. The Punzi CDS game has caused the collapse of the housing market, the credit market bubble to burst, the airline industry to down size, the cost of household goods to rise and inflated of the US dollar. Indeed. the speculation in CDS has destabilized the world economy. World bankers are contemplating changing the current banking system of the world and moving out of swapping. For more detailed information about CDS click more CDS |

Enron created some $2.4 billion in credit notes that were underwritten by Citigroup, a Protection Seller of insurance. Credit-linked notes are a form of default insurance that, unlike a swap, can be sold to multiple speculators [ “ like passing the buck.” ]

Enron created some $2.4 billion in credit notes that were underwritten by Citigroup, a Protection Seller of insurance. Credit-linked notes are a form of default insurance that, unlike a swap, can be sold to multiple speculators [ “ like passing the buck.” ]